Most professional actors, musicians, artists, or other entertainers contract their services through a so-called “Loan-Out Company.” We sat down with entrepreneur/actor Kevin L. Walker to hash out the details involving Loan Outs for actors/actresses, influencers, entertainers, producers, etc., for an article he’s featuring on his Hindsight Advice E-learning resource for Artists and Entrepreneurs.

There is a lot of confusion amongst industry professionals about the reason(s) behind establishing a “Loan-Out”Company, or whether establishing a Loan-Out Company is even a good idea at all for their circumstances.

Walker began the discussion by saying, “Remember, taxes and interest are to be legally avoided whenever possible. Doing so is like a cheat code to building wealth. Thus, it is ALL LEGAL. ”

What is a “Loan-Out” Company?

A Loan-Out Company is a separate business “entity” (e.g. a corporation or LLC) established for the purpose of “loaning out” the services of its owner/employee to third parties.

For example, the Loan-Out Company of a musician “loans out”/offers the musician’s services (recording, production, live performance, etc.) by entering into contracts with the end users of those services, whether a record label, a music publishing company, or concert venue.

What is a “Pass Through” Entity/Loan Out Company?

A pass–through entity is a special business structure that is used to reduce the effects of double taxation. Pass–through entities don’t pay income taxes at the corporate level. Instead, corporate income is allocated among the owners, and income taxes are only levied at the individual owners’ level.

Simplified: Pass through entity such as S corps, do not pay any federal income tax. All remaining profit or loss ir passed through to the owner(s) then taxed. In comparison, a C corp would be taxed federal income tax on a company level, the owner(s) are taxed again.

What Is the Self-employment Tax Rate?

You have to pay taxes on your total net earnings every year. For self-employment income earned in a particular year, the self-employment tax rate is 15.3%.

The rate consists of two parts: 12.4% for Social Security (old-age, survivors, and disability insurance) and 2.9% for Medicare (hospital insurance).

The Social Security portion is capped at a maximum amount, which changes each year. If your net earnings exceed the maximum that that year, you continue to pay only the Medicare portion of the SECA tax.

How does that compare to a W2 employee?

The 2018 Federal tax bracket for a married filing jointly couple earning $100,000 is 22%. The 2018 New Jersey tax bracket for a married filing jointly couple earning $100,000 is 5.53%

That means a W2 employee is paying a total tax rate is 27.53% not counting deductions to keep things simple, compared to just 15.3% for a self-employed person. How does it compare? It doesn’t. You shouldn’t need any more convincing to start your own business.

When Should I Form a Loan Out Company?

Common recommendations I hear from managers and agents to most entertainers is, a Loan-Out Company is only worth considering once he or she is consistently generating a certain level of income. A typically prescribed threshold being at least $75,000-$100,000 per year however, having an entity from the start can be beneficial if you are generating at least $800 of business revenue per year.

If you have a hobby that generates revenue, you have a business. Starting a business that with just a few hours of work a week, can easily make you $1,000 a month within a year, and bringing in some extra money is far from the only incentive to start a small business.

The US economy is driven by small businesses, and our tax law is set up to incentivize and reward business owners. Many of us knew that, but the numbers might surprise you. Almost 100% of US employment firms are made up of small businesses, 99.7%.

There are 5.9 million firms with at least one employee and 3.6 million with fewer than five employees. There are less than 20,000 companies in the US that employ more than 500 people.

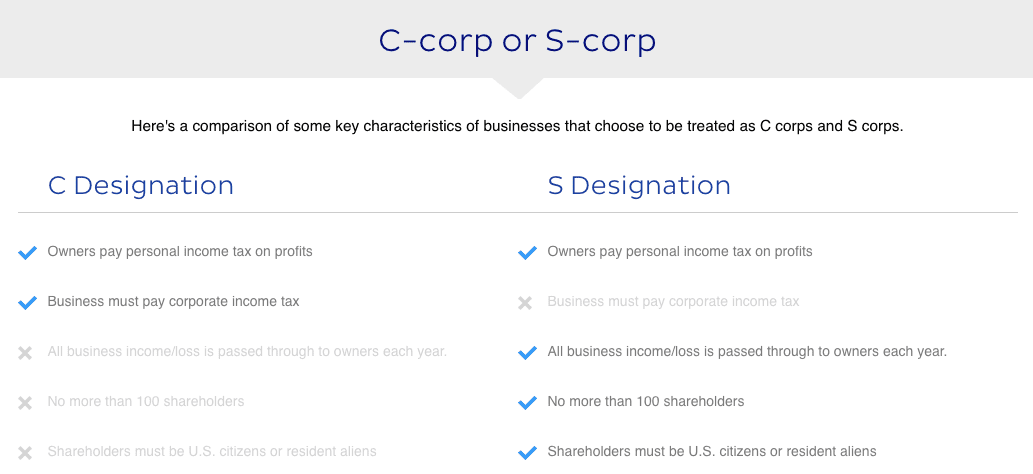

LC vs S Corp

LLC’s and S Corp’s have some similarities and some key differences.

Similarities

- Limited liability protection. Business owners are generally not personally responsible for business debts and liabilities.

- Separate entities. LLC’s and S Corp’s are separate legal entities created by filing papers with the state.

- Pass-through taxation. Both are generally pass-through tax entities, but S corps must file a business tax return. An LLC must only file a business tax return if there is more than one owner.

- Ongoing state requirements. Both are subject to state-mandated requirements, like filing annual reports and paying the required fees.

Differences

- Members: LLCs can have any number of members; S corps must have 100 shareholders or fewer.

- Citizenship/Residency: LLC members don’t have to be US citizens or residents. S Corp shareholders must be citizens or residents.

- Self-employment taxes: This is the big one guys. S Corps have more advantageous self-employment taxes than LLC’s. S Corp owners can be considered employees and paid “a reasonable salary.” FICA taxes are taken out and paid on the amount of the salary. Corporate earnings after salary may be able to be treated as unearned income that will not be subject to self-employment taxes.

Starting as an LLC and LATER Being taxed as an S Corp

There is an area in the battle between LLC vs. an S Corp where the S Corp is a clear winner.

The self-employment taxes are the significant benefit to having an S Corp over an LLC but because an LLC is so much simpler, start there. You can then later elect to have your entity taxed as an S Corp by filing a form 2553.

Purpose of Form

A corporation or other entity eligible to elect to be treated as a corporation must use Form 2553 to make an election under section 1362(a) to be an S corporation. An entity eligible to elect to be treated as a corporation that meets certain tests discussed below will be treated as a corporation as of the effective date of the S corporation election and doesn’t need to file Form 8832, Entity Classification Election.

The income of an S corporation generally is taxed to the shareholders of the corporation rather than to the corporation itself. However, an S corporation may still owe tax on certain income. For details, see Tax and Payments in the Instructions for Form 1120S, U.S. Income Tax Return for an S Corporation.

Who May Elect

A corporation or other entity eligible to elect to be treated as a corporation may elect to be an S corporation only if it meets all the following tests.

- It is (a) a domestic corporation, or (b) a domestic entity eligible to elect to be treated as a corporation, that timely files Form 2553 and meets all the other tests listed below. If Form 2553 isn’t timely filed, see Relief for Late Elections, later.

- It has no more than 100 shareholders. You can treat an individual and his or her spouse (and their estates) as one shareholder for this test. You can also treat all members of a family (as defined in section 1361(c)(1)(B)) and their estates as one shareholder for this test. For additional situations in which certain entities will be treated as members of a family, see Regulations section 1.1361-1(e)(3)(ii). All others are treated as separate shareholders. For details, see section 1361(c)(1).

- Its only shareholders are individuals, estates, exempt organizations described in section 401(a) or 501(c)(3), or certain trusts described in section 1361(c)(2)(A).For information about the section 1361(d)(2) election to be a qualified subchapter S trust (QSST), see the instructions for Part III. For information about the section 1361(e)(3) election to be an electing small business trust (ESBT), see Regulations section 1.1361-1(m). For guidance on how to convert a QSST to an ESBT, see Regulations section 1.1361-1(j)(12). If these elections weren’t timely made, see Rev. Proc. 2013-30, 2013-36 I.R.B. 173, available at IRS.gov/irb/2013-36_IRB#RP-2013-30.

- It has no nonresident alien shareholders.

- It has only one class of stock (disregarding differences in voting rights). Generally, a corporation is treated as having only one class of stock if all outstanding shares of the corporation’s stock confer identical rights to distribution and liquidation proceeds. See Regulations section 1.1361-1(l) for details.

- It isn’t one of the following ineligible corporations.

- A bank or thrift institution that uses the reserve method of accounting for bad debts under section 585.

- An insurance company subject to tax under subchapter L of the Code.

- A corporation that has elected to be treated as a possessions corporation under section 936.

- A domestic international sales corporation (DISC) or former DISC.

- It has or will adopt or change to one of the following tax years.

- A tax year ending December 31.

- A natural business year.

- An ownership tax year.

- A tax year elected under section 444.

- A 52-53-week tax year ending with reference to a year listed above.

- Any other tax year (including a 52-53-week tax year) for which the corporation establishes a business purpose.

For details on making a section 444 election or requesting a natural business, ownership, or other business purpose tax year, see the instructions for Part II.

- Each shareholder consents as explained in the instructions for column K.

See sections 1361, 1362, and 1378, and their related regulations for additional information on the above tests.

A parent S corporation can elect to treat an eligible wholly owned subsidiary as a qualified subchapter S subsidiary. If the election is made, the subsidiary’s assets, liabilities, and items of income, deduction, and credit generally are treated as those of the parent. For details, see Form 8869, Qualified Subchapter S Subsidiary Election.

When To Make the Election

Complete and file Form 2553:

- No more than 2 months and 15 days after the beginning of the tax year the election is to take effect, or

- At any time during the tax year preceding the tax year it is to take effect.

For this purpose, the 2-month period begins on the day of the month the tax year begins and ends with the close of the day before the numerically corresponding day of the second calendar month following that month. If there is no corresponding day, use the close of the last day of the calendar month.

Example 1. No prior tax year.

A calendar year small business corporation begins its first tax year on January 7. The 2-month period ends March 6 and 15 days after that is March 21. To be an S corporation beginning with its first tax year, the corporation must file Form 2553 during the period that begins January 7 and ends March 21. Because the corporation had no prior tax year, an election made before January 7 won’t be valid.

Example 2. Prior tax year.

A calendar year small business corporation has been filing Form 1120 as a C corporation but wishes to make an S election for its next tax year beginning January 1. The 2-month period ends February 28 (29 in leap years) and 15 days after that is March 15. To be an S corporation beginning with its next tax year, the corporation must file Form 2553 during the period that begins the first day (January 1) of its last year as a C corporation and ends March 15th of the year it wishes to be an S corporation. Because the corporation had a prior tax year, it can make the election at any time during that prior tax year.

Example 3. Tax year less than 2 1/2 months.

A calendar year small business corporation begins its first tax year on November 8. The 2-month period ends January 7 and 15 days after that is January 22. To be an S corporation beginning with its short tax year, the corporation must file Form 2553 during the period that begins November 8 and ends January 22. Because the corporation had no prior tax year, an election made before November 8 won’t be valid.

Relief for Late Elections

The following two sections discuss relief for late S corporation elections and relief for late S corporation and entity classification elections for the same entity. For supplemental procedural requirements when seeking relief for multiple late elections, see Rev. Proc. 2013-30, section 4.04.

When filing Form 2553 for a late S corporation election, the corporation (entity) must enter in the top margin of the first page of Form 2553 “FILED PURSUANT TO REV. PROC. 2013-30.” Also, if the late election is made by attaching Form 2553 to Form 1120S, the corporation (entity) must enter in the top margin of the first page of Form 1120S “INCLUDES LATE ELECTION(S) FILED PURSUANT TO REV. PROC. 2013-30.”

The election can be filed with the current Form 1120S if all earlier Forms 1120S have been filed. The election can be attached to the first Form 1120S for the year including the effective date if filed simultaneously with any other delinquent Forms 1120S. Form 2553 can also be filed separately.

Relief for a Late S Corporation Election Filed by a Corporation

A late election to be an S corporation generally is effective for the tax year following the tax year beginning on the date entered on line E of Form 2553. However, relief for a late election may be available if the corporation can show that the failure to file on time was due to reasonable cause.

To request relief for a late election, a corporation that meets the following requirements must explain the reasonable cause for failure to timely file the election and its diligent actions to correct the mistake upon discovery. This information can be provided on line I of Form 2553 or on an attached statement.

- The corporation intended to be classified as an S corporation as of the date entered on line E of Form 2553;

- The corporation fails to qualify as an S corporation (see Who May Elect, earlier) on the effective date entered on line E of Form 2553 solely because Form 2553 wasn’t filed by the due date (see When To Make the Election, earlier);

- The corporation has reasonable cause for its failure to timely file Form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file Form 2553;

- Form 2553 will be filed within 3 years and 75 days of the date entered on line E of Form 2553; and

- A corporation that meets requirements (1) through (4) must also be able to provide statements from all shareholders who were shareholders during the period between the date entered on line E of Form 2553 and the date the completed Form 2553 is filed stating that they have reported their income on all affected returns consistent with the S corporation election for the year the election should have been made and all subsequent years. Completion of Form 2553, Part I, column K, Shareholder’s Consent Statement (or similar document attached to Form 2553), will meet this requirement; or

- A corporation that meets requirements (1) through (3) but not requirement (4) can still request relief for a late election on Form 2553 if the following statements are true.

- The corporation and all its shareholders reported their income consistent with S corporation status for the year the S corporation election should have been made, and for every subsequent tax year (if any);

- At least 6 months have elapsed since the date on which the corporation filed its tax return for the first year the corporation intended to be an S corporation; and

- Neither the corporation nor any of its shareholders was notified by the IRS of any problem regarding the S corporation status within 6 months of the date on which the Form 1120S for the first year was timely filed.

To request relief for a late election when the above requirements aren’t met, the corporation generally must request a private letter ruling and pay a user fee in accordance with Rev. Proc. 2017-1, 2017-1 I.R.B. 1 (or its successor).

Relief for a Late S Corporation Election Filed By an Entity Eligible To Elect To Be Treated as a Corporation

A late election to be an S corporation and a late entity classification election for the same entity may be available if the entity can show that the failure to file Form 2553 on time was due to reasonable cause. Relief must be requested within 3 years and 75 days of the effective date entered on line E of Form 2553.

To request relief for a late election, an entity that meets the following requirements must explain the reasonable cause for failure to timely file the election and its diligent actions to correct the mistake upon discovery. This information can be provided on line I of Form 2553 or on an attached statement.

- The entity is an eligible entity as defined in Regulations section 301.7701-3(a) (see Purpose of Form in the Form 8832 instructions).

- The entity intended to be classified as an S corporation as of the date entered on line E of Form 2553.

- Form 2553 will be filed within 3 years and 75 days of the date entered on line E of Form 2553.

- The entity failed to qualify as a corporation solely because Form 8832 wasn’t timely filed under Regulations section 301.7701-3(c)(1)(i) (see When To File in the Form 8832 instructions), or Form 8832 wasn’t deemed to have been filed under Regulations section 301.7701-3(c)(1)(v)(C) (see Who Must File in the Form 8832 instructions).

- The entity fails to qualify as an S corporation (see Who May Elect, earlier) on the effective date entered on line E of Form 2553 because Form 2553 wasn’t filed by the due date (see When To Make the Election, earlier).

- The entity either:

- Timely filed all Forms 1120S consistent with its requested classification as an S corporation, or

- Didn’t file Form 1120S because the due date for the first year’s Form 1120S hasn’t passed.

- The entity has reasonable cause for its failure to timely file Form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file Form 2553.

- The S corporation can provide statements from all shareholders who were shareholders during the period between the date entered on line E of Form 2553 and the date the completed Form 2553 is filed stating that they have reported their income on all affected returns consistent with the S corporation election for the year the election should have been made and all subsequent years. Completion of Form 2553, Part I, column K, Shareholder’s Consent Statement (or similar document attached to Form 2553), will meet this requirement.

To request relief for a late election when the above requirements aren’t met, the entity generally must request a private letter ruling and pay a user fee in accordance with Rev. Proc. 2017-1 (or its successor).

How Do I Form a Loan-Out Company?

Establishing a Loan-Out Company is the same as forming a standard LLC or corporation. You must comply with state filing requirements, which can include filing articles of organization with the state, preparing your company’s operating documents (Bylaws, Operating Agreement, etc.), issuing shares or interests (if applicable), and obtaining a EIN/Tax ID number.

Protections & Benefits of an Entity/”Loan Out Company”

1) Asset Protection

Once an entity is formed, from that point on, prospective employers will hire that “Loan-Out Company,” not the individual. However, hiring parties can require that the principal also personally enter into an “inducement” agreement. This is typically a paragraph, tacked onto the end of a contract, that generally states that if anything should happen to the Loan-Out Company, the individual will still provide the agreed-upon service(s).

People with a strong brand, or leverage-able assets can most likely avoid signing an inducement, but “non-superstars” should expect to abide by this requirement.

The Loan-Out Company is a separate legal entity, so property held in the name of its owners cannot be used to repay the debts of the company, or be used to satisfy a judgment against the company. That means, if your company gets sued, someone can’t come after your personal assets as a result. Take, for example, a situation where your company has $5,000 in its account, its owner has $10,000 in his personal bank account, and the company gets sued for $10,000 and loses. If the $5,000 is the only asset the company has, the winner of the lawsuit cannot come after the owner for the remaining $5,000 that the company would still owe.

2) Tax Savings

There may be tax advantages for the principal to take a consistent, smaller salary, rather than having any money immediately pass through to the owner/employee. If you are not comfortable calculating the differences on your own, you should consult with a tax professional before deciding on which structure would better suit your specific circumstances.

A Loan-Out Company may also see tax savings that would not be available to a musician if he or she is providing services without one.

First, Loan-Out Companies are a great way to reduce tax exposure. Businesses are allowed to subtract expenses from their calculations of income, while individuals are not. There are, however, various deductions available to individuals, such as the “home office deduction,” but these are only partial write-offs, allowing you to subtract only a portion of these expenses from your taxable income.

Retirement Benefits

You might feel pretty lucky to have an employer-sponsored 401k at your job and a Roth IRA, but the retirement account benefits to having your own business are infinitely better!

SEP IRA

The SEP IRA is a monstrous tax cheat code. It’s a way for the self-employed who don’t have access to an employer-sponsored 401k to save for retirement. A SEP IRA has a much higher contribution limit than a Roth IRA and is much more flexible than a 401k.

A business owner can contribute up to $53,000 per year. The 2018 limit for Roth contributions is a meager $5,500. Owners can deduct 100% of that $53,000 from their business earnings.

This contribution is essentially pre-tax, and you can invest in pretty much anything including rental property, unlike a 401k which is limited to the funds your employer offers many of which often have very high fees which eat up your retirement savings.

IRA’s and 401k

You still can potentially qualify for the regular IRA’s, Traditional and Roth, and you can even run a 401k through your company bringing your potential tax-advantaged earnings to:

- $53,000 for a SEP IRA – tax-deferred.

- If you qualify, you can contribute up to $5,500 to a regular Roth or Traditional IRA.

- Your business can match 100% of 401k contributions you make up to 3% of your salary. On $100k that’s $3,000 from you and $3,000 from your business all tax-deferred

Vanguard shows you all of their retirement accounts available to small business owners.

Main Costs of a “Loan-Out” Company

While the advantages to forming a Loan-Out Company may be significant, there are additional costs and expenses associated with forming and maintaining a business entity, and the tax consequences if one doesn’t do so correctly can be substantial.

1) Fees to Form

Forming a Loan-Out Company is no different from forming any other LLC or corporation. It begins with filing the company’s Articles of Organization with the state, the fee for which varies by states. For example, in New York, the state filing fee to form an LLC is $200 plus attorney’s fees, where California’s filing fee to form an LLC is only $70.

Additionally, there may be minimum state taxes ($800 in California), and other small filing fees due within a few months after the company is established.

2) Annual Operating Expenses/Maintaining Business Entity

A Loan-Out Company must maintain its status by making annual filings and tax payments to the state in which it was formed, and possibly to other states where it conducts operations. For example, a Delaware LLC whose owner is an artist with homes in New York and California, where he or she renders substantially all of his or her services, will be required to “qualify” in those states as well. That means that the artist will have to pay certain fees to register in New York and California, and pay taxes to New York and California based on the income generated in each state.

Another expense that many “green” artists don’t think about is expense is unemployment insurance, which may be necessary if you get injured and can no longer provide services and generate an income. In order to maintain unemployment insurance, you will need to pay yourself a fair wage or salary, which means that a portion of your revenue must be set allocated to pay yourself, including the amounts needed for traditional withholdings and deductions.

Cautions on “Tax Avoidance”

The IRS is against the use of Loan-Out Companies strictly as a tax avoidance device. Therefore, if the company isn’t properly documented and used consistently, one may find the IRS taking the position that a Loan-Out Company is simply a tax avoidance scheme, and disregard it for tax purposes. This means that you could find yourself being charged the higher, personal tax rate, despite paying the different costs and expenses associated with forming your Loan-Out Company.

If the IRS deems it necessary to prevent tax avoidance, it has the authority to reallocate income between taxpayers sharing common ownership and control. Mostly, this occurs when the company is formed after the signing of the contracts for the artist’s services. Therefore, to minimize the risk, one should definitely form a Loan-Out Company prior to entering into a contract on its behalf.

Is there a Loan-Out Company in My Future?

As explained above, a properly structured Loan-Out Company can provide substantial tax and other benefits, but without proper planning and administration, business problems and additional expenses can outweigh the potential advantages. Many businesses turn to hiring a bookkeeper to assure they account properly, but you should consult with your tax advisor as well as an experienced entertainment lawyer before making any decision.